Ozempic Insurance Eligibility Estimator

Use this tool to estimate your likelihood of insurance coverage for Ozempic based on common payer criteria.

You have probably seen the headlines. Everyone wants Ozempic. But here is the hard truth: you cannot just walk into a pharmacy and buy it because you want to lose a few pounds or because your blood sugar was slightly high once. Insurance companies and doctors follow strict rules. The most common question patients ask is about their A1C level. So, what does your A1C need to be to get Ozempic?

The short answer is that there is no single universal number that guarantees approval. However, most insurance plans require an A1C of 7.0% or higher to cover the medication for type 2 diabetes. If you are looking at it for weight loss, the rules change completely. Let’s break down how this works in practice.

Understanding the A1C Threshold for Diabetes

To understand why insurers care about your A1C, you first need to know what A1C actually measures. Your A1C test shows your average blood sugar levels over the past two to three months. It is expressed as a percentage. For most people without diabetes, an A1C below 5.7% is considered normal. Between 5.7% and 6.4% is prediabetes. At 6.5% or higher, you are diagnosed with diabetes.

Ozempic is a brand name for semaglutide, a GLP-1 receptor agonist originally approved by the FDA for treating type 2 diabetes. Because it is expensive-often costing over $900 per month without insurance-payers use "step therapy" protocols. This means they want proof that cheaper options failed before they pay for the big gun.

For type 2 diabetes coverage, here is the typical landscape:

- A1C below 7.0%: Most insurance plans will deny coverage for Ozempic if your A1C is well-controlled on other medications like metformin. They argue you do not need a stronger drug yet.

- A1C between 7.0% and 8.0%: This is the gray zone. Some plans may approve it if you have tried at least two other oral medications (like metformin and a DPP-4 inhibitor) without success.

- A1C above 8.0%: Approval becomes much more likely. High A1C indicates poor control, which increases the risk of complications like nerve damage, kidney issues, and vision problems. Insurers see Ozempic as a necessary intervention to prevent these costly long-term health issues.

Your doctor will likely need to submit a Prior Authorization form. This document proves that you meet the clinical criteria. Simply having a high A1C might not be enough; you also need to show that lifestyle changes and first-line treatments haven’t worked.

| A1C Range | Clinical Status | Insurance Coverage Chance | Typical Requirement |

|---|---|---|---|

| Below 7.0% | Controlled / Prediabetes | Very Low | Usually denied for diabetes indication |

| 7.0% - 8.0% | Moderately Uncontrolled | Moderate | Requires failure of 2+ other meds |

| Above 8.0% | Poorly Controlled | High | Easier prior authorization approval |

Ozempic vs. Wegovy: The Weight Loss Loophole

Here is where things get confusing. You might hear friends talking about using Ozempic for weight loss even though their A1C is perfect. Technically, Ozempic is not approved for weight loss alone. That is what Wegovy is for. Wegovy contains the exact same ingredient-semaglutide-but at a higher maximum dose (2.4 mg vs. 2.0 mg for Ozempic).

If your goal is purely weight management and you do not have type 2 diabetes, your A1C doesn’t matter for eligibility. Instead, your Body Mass Index (BMI) does. To qualify for Wegovy (or off-label Ozempic for weight), you generally need:

- A BMI of 30 or higher (classified as obese).

- A BMI of 27 or higher with at least one weight-related condition, such as high blood pressure, type 2 diabetes, or high cholesterol.

Many patients try to get Ozempic prescribed off-label for weight loss because it is sometimes easier to find in stock than Wegovy. However, insurance rarely covers this. You would likely have to pay out of pocket. In 2026, the cash price can still be steep, so many people turn to patient assistance programs or specialized online pharmacies that offer discounts.

It is worth noting that while we focus heavily on medical metrics, the healthcare journey often intersects with broader lifestyle needs. For instance, individuals managing chronic conditions sometimes seek comprehensive support networks beyond just medication. While this article focuses on diabetes metrics, resources like this directory exist for different personal needs in other regions, highlighting how diverse service directories can be compared to rigid medical guidelines.

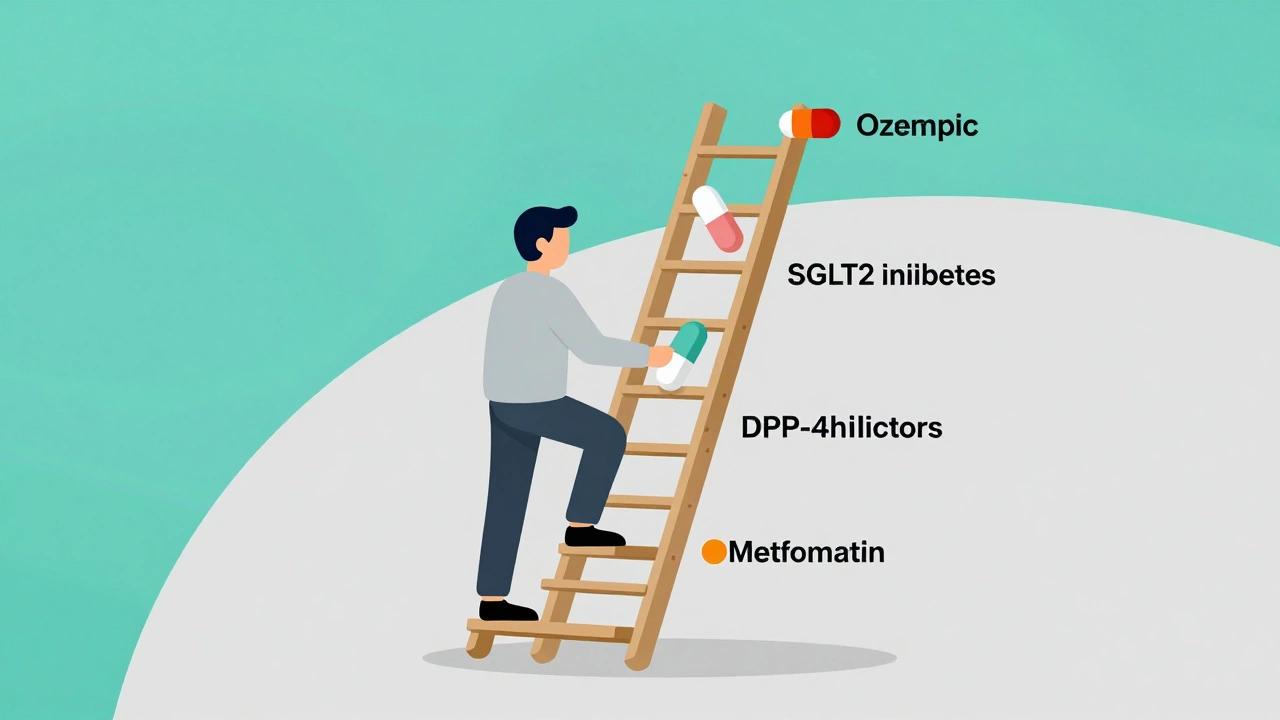

The Step Therapy Process: Why Your Doctor Says "No" First

Even if your A1C is 9%, your doctor might not prescribe Ozempic immediately. This isn’t because they don’t want to help you. It is because of step therapy. Insurance companies force doctors to try cheaper drugs first. Here is the typical ladder you must climb:

- Metformin: This is almost always the first line of defense. It is cheap, effective, and has decades of safety data. If you haven’t tried metformin, insurance will almost certainly deny Ozempic.

- DPP-4 Inhibitors: Drugs like Januvia (sitagliptin) or Tradjenta (linagliptin). These are oral pills that are less potent than injectables but cheaper.

- SGLT2 Inhibitors: Medications like Jardiance (empagliflozin) or Farxiga (dapagliflozin). These help your kidneys remove sugar through urine.

- Other Injectables: Sometimes insurers require you to try older GLP-1 agonists like Victoza or Trulicity before approving Ozempic.

Only after you fail these steps-or if you have a documented intolerance to them-will the insurance company consider Ozempic. This process can take months. During this time, your A1C might remain high, which is frustrating for patients who know Ozempic could work better for them.

How to Improve Your Chances of Approval

If you are stuck in the denial loop, there are strategies you can use. Working closely with your endocrinologist is key. Here is what helps:

- Document Side Effects: If metformin gave you severe stomach upset or neuropathy, make sure this is in your medical records. Intolerance is a valid reason to skip steps.

- Show Cardiac Risk Factors: Recent studies show semaglutide reduces the risk of heart attack and stroke. If you have existing cardiovascular disease, your doctor can appeal the insurance decision based on cardiac protection, not just blood sugar control.

- Appeal the Denial: Don’t accept the first "no." Ask your doctor to file a peer-to-peer review. This allows your doctor to speak directly with the insurance company’s medical director to argue your case.

Cost Considerations and Alternatives

If insurance denies coverage, the cost barrier is real. Without insurance, a month’s supply of Ozempic can range from $800 to $1,300 depending on the pharmacy and dosage. This is unsustainable for most people.

In 2026, several alternatives have emerged:

- Generic Semaglutide: As patents expire, generic versions are starting to appear in some markets, though availability varies by country.

- Tirzepatide (Mounjaro/Zepbound): This is a newer dual-agonist that some patients find more effective than semaglutide for both glucose control and weight loss. Insurance rules for Mounjaro are similar to Ozempic.

- Patient Assistance Programs: Novo Nordisk, the maker of Ozempic, offers coupons and assistance programs for eligible uninsured or underinsured patients. This can lower the monthly cost to around $25-$50.

Always check if your local pharmacy participates in these programs. Some online telehealth platforms also offer bundled pricing that includes the consultation and the medication, which can sometimes be cheaper than going through traditional insurance channels if you are paying out of pocket.

Common Mistakes Patients Make

I see patients making the same errors repeatedly. Avoid these pitfalls:

- Assuming One Size Fits All: Your friend’s A1C of 7.5% got approved, but yours didn’t. Every insurance plan has different formularies. What works for Blue Cross might not work for Aetna.

- Ignoring Lifestyle Changes: Insurers look at whether you are actively trying diet and exercise. If your records show no engagement with nutrition counseling, they may deny claims based on lack of effort.

- Not Tracking Progress: Keep a log of your blood sugar readings. Bring this data to your doctor. Concrete numbers showing consistent highs despite medication adherence are powerful evidence for prior authorization.

When to See a Specialist

If your primary care physician is struggling to get your insurance to approve Ozempic, consider seeing an endocrinologist. Specialists often have more experience navigating complex insurance appeals. They understand the specific language insurers use to deny or approve claims. They can also assess if you are a candidate for clinical trials or newer therapies that might bypass standard step therapy requirements.

Remember, the goal is not just to get the drug. The goal is to control your diabetes and protect your long-term health. Ozempic is a powerful tool, but it is not magic. It works best when combined with dietary changes, regular physical activity, and consistent monitoring.

Can I get Ozempic if my A1C is below 7%?

Generally, no. Most insurance plans require an A1C of 7.0% or higher to cover Ozempic for type 2 diabetes. If your A1C is lower, they will likely insist you stay on current medications unless you have other compelling medical reasons, such as significant weight loss needs or cardiovascular risks, and even then, coverage is not guaranteed.

Does Ozempic work for prediabetes?

While Ozempic can lower blood sugar in people with prediabetes, it is rarely prescribed for this condition due to cost and side effects. Doctors usually recommend lifestyle changes, metformin, or weight loss programs first. Insurance will almost never cover Ozempic for prediabetes alone.

How long does prior authorization take?

Prior authorization can take anywhere from a few days to several weeks. If your initial request is denied, filing an appeal can add another 2-4 weeks. It is important to start this process early so you do not run out of medication during the wait.

Is Wegovy covered if I have diabetes?

This depends on your insurance plan. Some plans cover Wegovy for weight loss if you have obesity-related conditions, including diabetes. Others may only cover Ozempic for diabetes and Wegovy for weight loss separately. Check your specific formulary to see which drug is preferred.

What if I can't afford Ozempic without insurance?

If you cannot afford Ozempic, look into the Novo Nordisk Patient Assistance Program. You can also ask your doctor about alternative GLP-1 agonists that might be cheaper or covered by your insurance. Generic semaglutide is becoming available in some regions, offering a lower-cost option.